Dive Brief:

- Nearly two-thirds of consumers in the U.S. who lean on buy now, pay later transactions to pay for goods and services take out multiple BNPL loans at once, the Consumer Financial Protection Bureau concluded in a study released Monday.

- Most people who use BNPL as a payment method also carry disproportionately large amounts of other types of debt such as credit card and personal debt, the bureau’s research showed.

- The majority of consumers who use BNPL (61%) have subprime or deep subprime credit scores, the report found. A FICO score between 580 and 619 is considered subprime, whereas a FICO score below 580 is considered deep subprime, according to the CFPB.

Dive Insight:

The CFPB analyzed 145 million buy now, pay later loan applications made from 2017 through 2022, and looked at factors like consumers’ credit score and spending history, the report said.

The average number of transactions per borrower increased from 8.5 in 2021 to 9.5 in 2022. And in 2022, 63% of borrowers took out more than one BNPL loan at a time, and 33% of borrowers who use BNPL took out loans from multiple companies.

Consumers who regularly use the payment method also hold more debt than those who do not, the CFPB found. Borrowers who took out at least one BNPL loan per month carry a balance of $453 more in personal loans and $871 more in credit card loans, among other debts, than consumers of the same age and similar credit scores who don't use buy now, pay later, the report said.

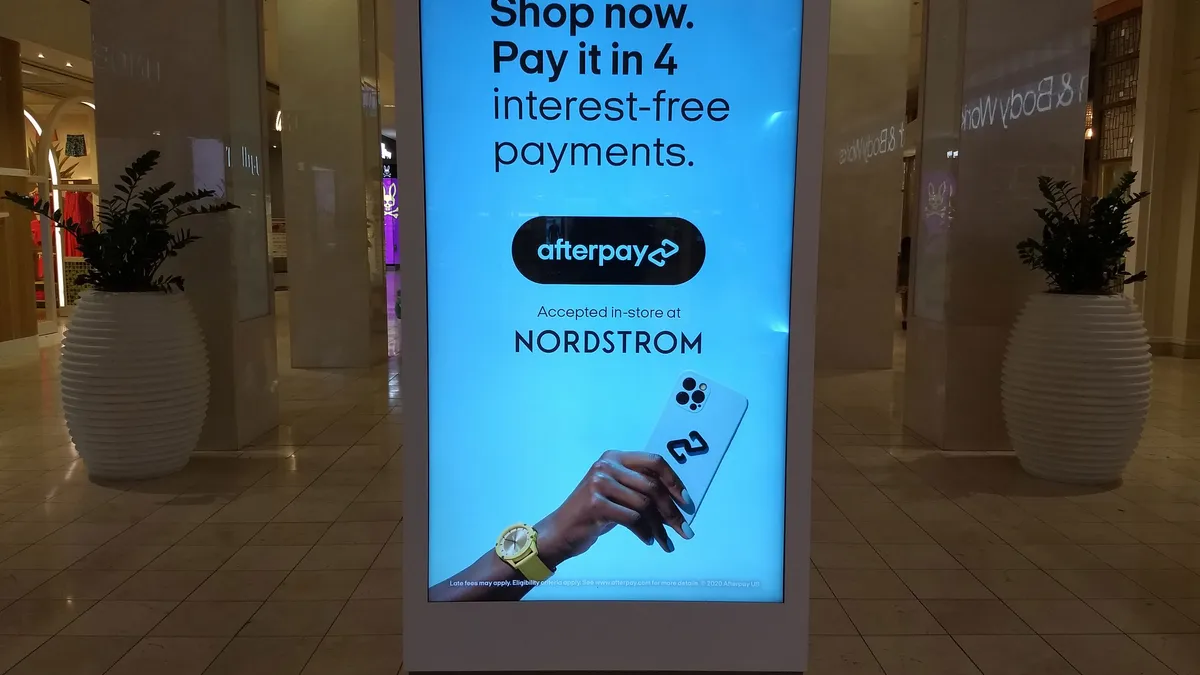

Lenders generally don't report buy now, pay later transactions to credit reporting agencies, the CFPB said in the report, so the bureau instead looked at a sample of BNPL applications from six companies: Affirm, Afterpay, Klarna, PayPal, Sezzle, and Zip.

BNPL companies have touted low default rates for consumers who use their services. The bureau's report found, on average, just 2% of borrowers defaulted on the transactions between 2019 and 2022 that it analyzed. It noted that’s likely related to consumers often setting up automatic repayment for buy now, pay later loans on credit cards and debit cards, meaning funds are automatically withdrawn from their account or added to their credit card balance.

Critics of the buy now, pay later industry say the repayment method encourages consumers to pile on more debt than they can reasonably repay.

One of those critics said the report validates many of his concerns.

“The data shows that BNPL is increasing access to credit for deep subprime consumers, even if they are facing escalating debt burdens elsewhere, and relying on ability-to-collect requirements rather than applying diligent underwriting standards," Adam Rust, director of financial services for the Consumer Federation of America, said in an email. “Today’s report should be a warning for everyone in light of how credit card balances are surging on household balance sheets.”

Industry representatives, on the other hand, maintain that by now, pay later is a valuable tool for consumers who have few other options.

BNPL serves as an alternative to more costly and riskier forms of credit, American Fintech Council CEO Phil Goldfeder told Payments Dive in an emailed statement.

“It’s easy for consumer groups and others to criticize when they don’t understand the nature of emerging financial products or the true needs of consumers across the country,” he said. “BNPL serves an alternative option to a predatory loan, pawn shops, overdraft fees or other financial tools that may not be as transparent, safe, or affordable.”

Buy now, pay later empowers consumers with “a responsible way to pay over time,” an Affirm spokesperson said in an emailed statement.

“Our success is aligned with consumers and responsibly extending access to credit that is repaid,” the statement said. “We will review the CFPB’s report and continue to engage with them as we do with all of our stakeholders.”

A spokesperson for Klarna declined to comment and spokespeople for the other four companies named in the report did not respond to messages seeking comment.